Once you’ve established your “20 Mile March,” how do you track your progress along your journey? The key tool is your personal balance sheet. Your balance sheet tracks your assets and liabilities so you know your net worth at any point in time. Here’s how it works:

Assets – Liabilities = Net Worth

Assets are everything you own of monetary value. Liabilities are debts that you owe to others. If you list everything you own (assets) and subtract everything you owe (liabilities), you get your net worth. Net worth is what’s available to help you reach your future financial goals, and it should grow steadily over time.

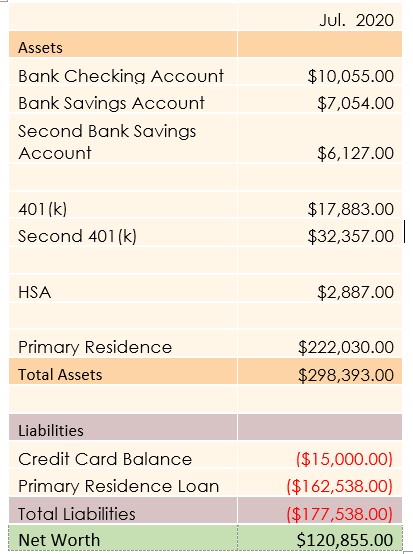

To determine your net worth, follow these steps (see Figure 1):

- List all of your financial assets (bank accounts, investment accounts, retirement accounts, real estate, etc.) and their current values. Add up these values.

- Next, list all of your liabilities (credit cards, student loans, auto loans, mortgage) and their current values. Add these up.

- Finally, subtract your total liabilities from your total assets to get your net worth.

Now, make observations.

- Is you net worth positive or negative? A positive net worth means you have more assets which can fund future goals. A negative net worth means you owe more than you own.

- How are your assets distributed? Do you have sufficient liquid assets (like cash) to meet emergencies? Is most of your wealth in long-term assets that you can’t access for many years, like retirement accounts? How much of your wealth is in fixed assets like real estate?

- How much of your debt is high interest debt such as credit card debt?

After making these observations, you can start creating strategy to balance short term needs with long-term goals. See our post on creating balance by prioritizing your cash flow.

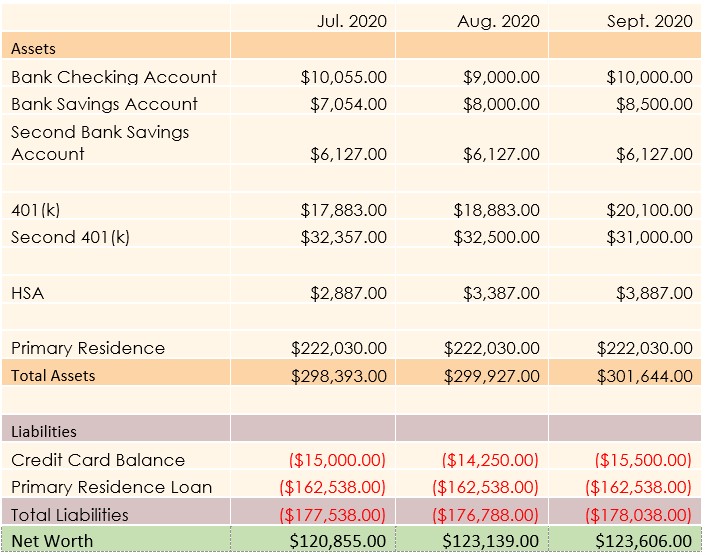

You can gain even more insight by observing changes in your net worth over time. On the last day of each month, sit down with a cup of coffee, your spreadsheet, and your month-end statements. Fill out your balance sheet monthly and observe trends. For example:

- Is your net worth changing from month to month? About how much does it change? Is it increasing or decreasing?

- What is driving this change—increased contributions to retirement accounts? Increased or decreased debt? Change in investment values or a combination?

Finally, create goals with your balance sheet

Once you start seeing patterns, start your 20 Mile March by establishing concrete goals. For example, set a goal to increase your net worth 10% a year and determine exactly where these changes can happen. Your net worth increases when you increase your assets (through savings or increased investment return) or decrease your liabilities by paying down debt.

In our next post, Financial Foundations 2: Cash Flow, we’ll discuss key strategies to increase net worth.