In our last post, Financial Foundations 1: Balance Sheet, we introduced the concept of net worth and showed you how to track your financial progress and set goals using a monthly balance sheet. Today, we’ll discuss how to reach these goals by tracking your cash flow.

Let’s say you have a goal of increasing your net worth by 10% each year. So, if your net worth is $100,000, you’ll need to increase it by $10,000 over twelve months.

You can increase net worth through:

- Saving more,

- Paying down debt, and

- Increasing return on investments.

The power behind this growth is your net cash flow–what’s left after you’ve made spending decisions. Basically:

Income – Expenses = Net Cash Flow

More About Net Cash Flow

Your net cash flow can be either positive or negative.

If the money you earn (your income) is more than the amount you spend (your expenses), you’ll have positive cash flow. You can add that excess cash to your savings and investments or use it to pay down debt.

If it’s negative, however, you’re either living off your savings or increasing debt, which are not good long-term strategies.

Sometimes negative cash flow isn’t a problem. For example, in retirement, we often use savings to meet expenses. If you have sufficient assets to pay these expenses, and that’s part of your long-term plan, then, it’s not a problem. But, if you’re unintentionally spending more than you earn, you won’t meet your long-term financial goals.

Track Cash Flow

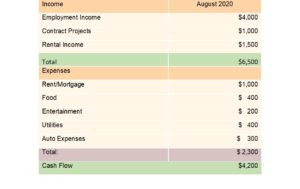

So, how do you track your cash flow? One way is to create a spreadsheet such as the one below. List your income for the month from all sources. This includes income from your primary job, other work, rental income, dividends and income from investments, etc. Then subtract all your expenses—from bank accounts, credit card statements, etc. Below is an example:

Here, August net cash was $6,500 – $2,300 or $4,200. That $4,200 can be used to increase savings or reduce debt, both of which will increase net worth. If the cash is added to an investment or retirement account, those assets will grow over time. Read our post on prioritizing cash flow to learn how best to use this excess cash.

Find the Patterns

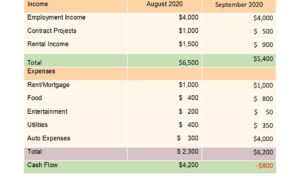

As with net worth, the key is to track over time and find patterns. Here’s a view over two months:

While August was a positive month, September was not, and we needed to use savings to meet expenses. Sometimes that happens in emergency situations, but hopefully it’s not happening regularly. In our example, over two months, net cash averaged a positive $3,600. Because each month is different, the key is to track spending monthly until you start recognizing patterns and can anticipate cash needs over periods of time.

Create an Action Plan

Once you have a general sense of monthly cash flow, you can start making intentional choices to achieve your net worth goal.

If you don’t want to manually enter all your expenses into a spreadsheet, you can track cash flow using a tool that aggregates your spending data like Mint (www.mint.com). Mint allows you to connect all of your accounts so that you can see all your data in one place. If you use online banking, your bank likely has a similar online service. Copper Seed can assist with this type of data aggregation as well. The key, however, is to easily see data over time in one place which is why a monthly spreadsheet can be so powerful in helping you see patterns over time.

In our next blog Financial Foundations 3: Don’t Give Up Your Mocha, we’ll explore ways to ensure positive cash flow consistently.